What Is an Endowment Assurance Plan? Common Misconceptions and What Investors Should Know

Introduction

“What is an endowment assurance plan?” is a common question among Singapore investors who prioritise capital stability, predictability, and structured outcomes. These plans have long formed part of Singapore’s insurance and financial planning landscape, offering a fixed maturity payout alongside life insurance protection. For conservative investors, understanding how such plans function is an important step before committing funds for the medium to long term.

Beyond their traditional role, endowment assurance plans also support a growing secondary market in Singapore. Some policyholders choose to exit before maturity due to changing financial priorities, allowing investors to acquire these policies through resale. When assessed carefully, this approach can shorten investment horizons and improve visibility over outcomes while retaining the contractual framework of what an endowment assurance plan is.

Misconceptions around guarantees, ownership, liquidity, and regulation often cloud investor judgement. This article clarifies how these plans work, addresses common misunderstandings, and outlines what investors should know when evaluating resale opportunities facilitated by Conservation Capital.

Key Takeaways:

- What is an endowment assurance plan and why do investors consider it?

An endowment assurance plan combines disciplined savings with insurance protection, offering a structured payout at maturity or upon death. It appeals to conservative investors seeking predictable outcomes rather than market-driven volatility.

- Why does an endowment assurance plan appear in the resale market?

Some policyholders exit their plans early due to changing financial needs. This creates resale opportunities where investors can acquire policies with accumulated value and shorter remaining tenures.

- Are returns from endowment assurance plans fully guaranteed?

Only the guaranteed portion of the payout is fixed. Bonuses are not assured and depend on insurer performance, economic conditions, and participating fund results.

- Why can resale policies offer clearer yield visibility?

Resale policies are often purchased below their accumulated value, with early penalties already absorbed and a shorter time to maturity, reducing uncertainty for incoming investors.

- Who are resale endowment policies most suitable for?

They are best suited for conservative investors with defined time horizons who prioritise capital stability, predictable payouts, and low-maintenance financial planning.

What Exactly Is an Endowment Assurance Plan?

At its foundation, an endowment assurance plan is a structured insurance contract that combines disciplined savings with protection. The policy pays out either at a fixed maturity date or upon the insured’s passing during the policy term. This dual structure explains why assurance plans differ from pure savings instruments in both cost and benefit composition.

These plans are issued and administered by insurers operating within Singapore’s regulated insurance framework. Even when ownership changes through resale, the insurer continues to administer the policy according to its original terms, preserving the integrity of what an endowment assurance plan is.

How Do Endowment Assurance Plans Typically Work?

To understand what an endowment assurance plan is, investors should recognise the commitment involved. Premiums are paid over a defined period, either fully paid upfront or across scheduled instalments. These contributions build guaranteed values and may also generate bonuses through the insurer’s participating fund.

When policyholders are unable or unwilling to continue, the policy may be surrendered or sold. Resale allows investors to step into an existing plan with accumulated value rather than starting from inception, which fundamentally changes the risk and return profile of what an endowment assurance plan is.

What Features Should Investors Expect?

A defining feature of what an endowment assurance plan is lies in the guaranteed portion of the payout. This component is contractually assured and insulated from short-term market fluctuations. In addition, non-guaranteed bonuses may be declared depending on insurer performance and long-term economic conditions.

Another important characteristic is the fixed maturity date. This allows investors to plan around education funding, retirement milestones, or capital preservation goals. When accessed through resale, these features typically remain intact, often with a shorter remaining tenure and clearer projected outcomes.

How Is It Different from Other Investment Products?

Understanding what an endowment assurance plan is becomes clearer when compared with other conservative options. Unlike equities or unit trusts, these plans offer low volatility and capital stability. Unlike Singapore Savings Bonds or Treasury Bills, they combine disciplined savings with insurance protection within a single structure.

For resale investors, this structure becomes more appealing because early-stage uncertainty and surrender penalties have already been absorbed by the original policyholder.

Why Endowment Assurance Plans Form the Basis of Traded Policies

The relevance of what an endowment assurance plan is in the secondary market lies in the value already embedded in these contracts. Traded policies are existing assurance plans transferred after several years of premium payments.

In Singapore, this secondary market revolves aroundtraded endowment policies, giving investors access to policies with established guaranteed values, accumulated bonuses, and shorter remaining terms. Conservation Capital evaluates these policies and facilitates secure transfers, allowing investors to access pre-built savings instruments at discounted entry points.

Common Misconceptions About Endowment Assurance Plans

Misunderstandings around endowment assurance plans often stem from oversimplified assumptions about guarantees, flexibility, and risk. Addressing these misconceptions allows investors to assess what an endowment assurance plan is with greater clarity, especially when comparing long-term commitments against resale or secondary market alternatives.

Misconception 1: Returns Are Always High and Fully Guaranteed

One of the most common misconceptions is that endowment assurance plans deliver high returns with no variability. While every plan includes a guaranteed component, the overall maturity value often comprises both guaranteed benefits and non-guaranteed bonuses.

These bonuses depend on factors such as insurer investment performance, prevailing interest rates, and long-term asset allocation decisions within the participating fund. As a result, projected returns shown in illustrations should be understood as estimates rather than fixed outcomes.

Misconception 2: You Can Exit Anytime Without Financial Impact

Endowment assurance plans are structured as long-term commitments designed to be held until maturity. Exiting early through surrender typically results in a payout that is lower than the total premiums paid, particularly in the earlier years of the policy. This is why some policyholders explore resale instead of surrender, as resale may allow them to realise more value from a policy that has already accumulated guaranteed benefits and bonuses.

This reinforces why truly understanding what an endowment assurance plan is matters before making early exit decisions.

Misconception 3: All Endowment Plans Are Structurally the Same

Not all endowment plans serve the same purpose. Endowment assurance plans include a life insurance component that provides a payout upon the insured’s death during the policy term. This protection element affects both pricing and benefit structure, distinguishing assurance plans from savings-only endowment plans. Investors comparing options should therefore consider whether they are prioritising pure savings, protection, or a combination of both.

Misconception 4: There Is No Risk at All

Although endowment assurance plans are generally considered low-risk compared to market-linked investments, they are not entirely risk-free. Only the guaranteed portion of the payout is fixed. Bonus declarations may vary over time and can be reduced or omitted during weaker economic conditions. Investors should factor this variability into their expectations rather than assuming that illustrated maturity values will always be achieved.

Misconception 5: These Plans Only Suit Very Long-Term Goals

Endowment assurance plans have traditionally been associated with long-term financial planning, such as retirement or legacy goals. However, many plans today fall within medium-term horizons, making them relevant for investors planning for education funding, capital preservation, or specific financial milestones.

This flexibility allows investors to align policy tenure more closely with their personal timelines rather than viewing these plans as inflexible, decades-long commitments.

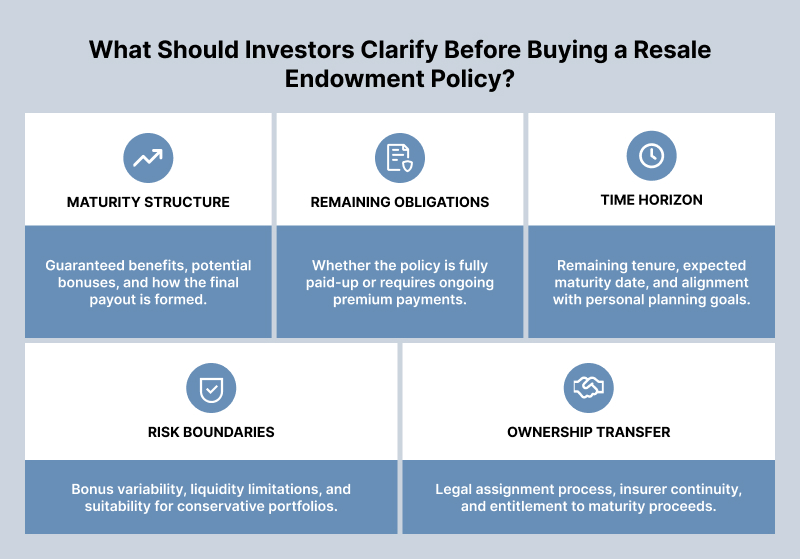

What Investors Should Know Before Considering One

A practical understanding of what an endowment assurance plan is involves recognising how payouts are formed, how resale changes the economics of the policy, and where limitations still apply. Investors benefit most when expectations around returns, timelines, and obligations are aligned upfront rather than discovered later in the process.

What Affects the Final Maturity Payout?

The final maturity payout is made up of guaranteed benefits and any bonuses declared by the insurer over the life of the policy. Guaranteed benefits are contractually defined, while bonuses depend on long-term insurer performance, prevailing interest rate conditions, and how the participating fund is managed. Consistent premium payments typically support stronger accumulated value, whereas changes to payment schedules may affect projections.

Premium Responsibilities After Resale

Understanding ongoing obligations is part of knowing what an endowment assurance plan is once ownership changes hands. Not all resale policies are fully paid-up at the point of transfer. Some contracts may still carry remaining premium obligations that the new owner must fulfil until the policy becomes paid-up or reaches maturity.

Investors should factor these ongoing cash flow commitments into their assessment, as they directly influence effective yield and suitability relative to other conservative instruments.

Why Resale Policies May Offer Higher Effective Yields

Resale transactions often allow investors to acquire policies at prices below their accumulated value. As the remaining tenure is shorter, the period of uncertainty is reduced and early-stage surrender penalties have already been absorbed by the original policyholder. This is why assurance plans accessed through resale endowment policies can provide clearer yield visibility compared to starting a new policy from inception.

Who Typically Benefits From Buying Pre-Owned Policies?

Pre-owned policies tend to suit conservative investors who prioritise predictability over growth volatility. For those evaluating what an endowment assurance plan is, these policies are commonly considered by individuals planning for education expenses, retirement milestones, or medium-term capital needs. Investors who prefer passive, low-maintenance instruments often value the defined maturity timeline and established policy value.

Who May Not Be Suitable

Despite their stability, these plans are not universally suitable. Investors who require liquidity before maturity may find the structure restrictive. Those uncomfortable with bonus variability or seeking market-linked upside may also find the risk-return profile misaligned with their objectives. Clear alignment between policy tenure and personal cash flow needs is essential.

Legal Ownership and Assignment

Legal assignment is a critical aspect of understanding what an endowment assurance plan is after it enters the resale market.

When a resale transaction takes place, ownership of the policy is transferred through absolute assignment. The investor becomes the legal policy owner, while the insurer remains unchanged and continues administering the policy under its original terms. Upon maturity, proceeds are paid directly by the insurer to the assigned owner, ensuring continuity and contractual clarity.

Process Timelines and Expectations

Administrative timelines further illustrate what an endowment assurance plan is as a contractual insurance product rather than a liquid investment.

Policy assignment is not immediate. Completion depends on documentation review and insurer processing requirements, which can take time. Investors should plan for administrative lead time between agreement and formal transfer, rather than assuming instant ownership or benefit entitlement.

How Conservation Capital Supports Investors in the Traded Policy Market

Conservation Capital provides structured access to resale opportunities grounded in endowment assurance plans, with a focus on clarity, suitability, and disciplined evaluation. Rather than treating resale as a one-size-fits-all solution, the emphasis is on helping investors understand how each policy fits within their financial timeline and risk preferences.

Transparent Policy Screening

Each policy is assessed across multiple dimensions, including insurer profile, surrender value, accumulated bonuses, remaining tenure, and premium structure. For investors seeking clarity on what an endowment assurance plan is, this screening process helps filter out policies with unfavourable characteristics, allowing them to focus on opportunities with clearer value visibility and more predictable maturity outcomes.

Secure Assignment Process

Ownership transfer is facilitated directly with insurers to ensure that legal documentation, policy records, and beneficiary entitlements are properly updated. Investors receive formal confirmation of assignment, providing clarity on ownership status and ensuring that the policy continues to be administered under its original contractual terms.

Matching Investors With Suitable Opportunities

Policies are aligned with investor objectives based on factors such as remaining duration, cash flow requirements, and planning horizons. By grounding recommendations in regulatory framework guidance and financial planning principles relevant to Singapore, Conservation Capital helps investors evaluate suitability rather than focusing solely on projected returns.

Clearer, More Predictable Outcomes

Because resale policies already carry built-in value, investors face less early-stage uncertainty compared to starting a new plan. The remaining term is known upfront, allowing for more accurate planning and positioning within a conservative portfolio, especially when compared with holding idle cash or committing to long-dated instruments with longer break-even periods.

Frequently Asked Questions

Is an endowment assurance plan the same as a traded or resale policy?

No. For investors seeking clarity on what an endowment assurance plan is, it refers to the original long-term savings and protection policy issued directly by an insurer. On the other hand, a traded or resale policy refers to an existing policy that a policyholder chooses to exit before maturity. Once the policy is legally transferred to a new investor, the incoming owner takes over the remaining tenure and future benefits. While the underlying policy structure remains unchanged, resale policies typically have shorter remaining durations and clearer visibility over accumulated value.

What types of endowment policies can be sold?

Policyholders may decide to sell their policies for various reasons, such as changes in financial priorities, cash flow constraints, or shifts in long-term planning objectives. In many cases, selling a policy allows the policyholder to realise more value than surrendering it directly to the insurer. This is why some policyholders choose to sell their endowment policy through resale channels rather than accept a lower surrender value, creating opportunities for investors to acquire policies with built-in value.

How do investors eventually receive their returns?

Investors receive their returns when the policy reaches maturity. At that point, the insurer pays the maturity proceeds directly to the assigned owner, based on the policy’s guaranteed benefits and any bonuses declared. Most investors plan to cash out their endowment policy at maturity rather than exiting early, as holding the policy to term typically preserves projected outcomes and avoids value erosion associated with early surrender.

Conclusion

A clear understanding of what constitutes an endowment assurance plan is essential for investors navigating Singapore’s resale policy market. Misconceptions often stem from uncertainty around guarantees, ownership, premiums, and timelines. When evaluated carefully, pre-owned assurance plans can offer structured outcomes, defined horizons, and lower volatility that align well with conservative financial planning.

Conservation Capital supports investors by sourcing quality policies, verifying accumulated value, and managing secure assignments with clarity and transparency. Speak with Conservation Capital to review available opportunities and assess suitability before making any commitment.